While the market today has become less competitive, many would-be buyers have stopped looking due to cost constraints. Mortgage application activity has declined substantially in recent months, returning to more typical historical levels. In the first quarter of 2020, prospective buyers submitted 1.26 million conventional conforming mortgage applications, and just over 660,000 were approved. Both of these figures approximately doubled by the peak of activity in the first quarter of 2021 before beginning to decline. The cooling of the market accelerated in 2022, and in the second quarter of last year, applications and approvals were both back below their pre-pandemic levels.

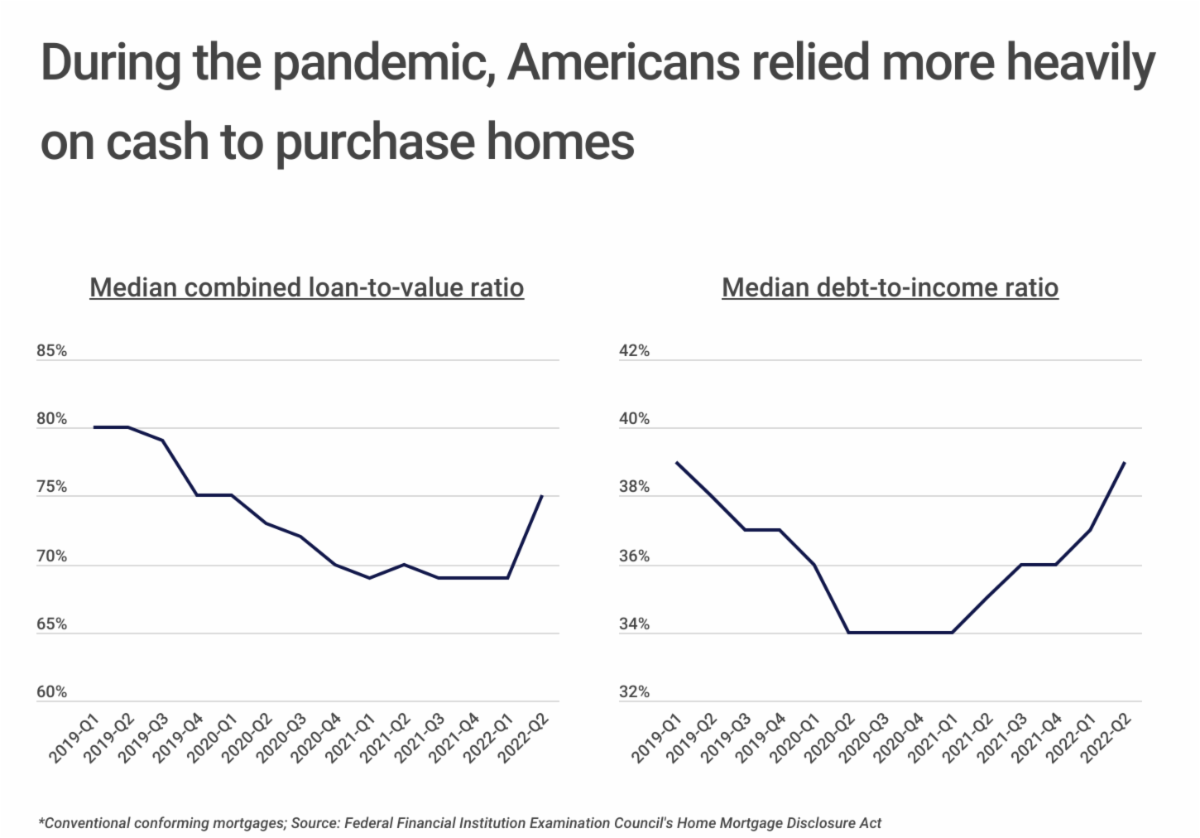

Amid this rapid rise and fall in mortgage applications and approvals, applicants’ mortgage qualifications shifted as well. Prior to the pandemic, the median combined loan-to-value ratio for U.S. mortgages was around 75%, meaning that the typical buyer put 25% down on a home. That figure fell to below 70% by the beginning of 2021 and remained there until rebounding back to 75% in the second quarter of 2022. A similar trend took place in debt-to-income ratio: after falling to a low of 34% in 2021, the median debt-to-income ratio for a mortgage applicant returned to its highest levels since 2019 after mortgage rates began increasing early last year. These figures suggest that buyers were using more of their own cash and personal savings to finance purchases during the pandemic. Flush with cash from increased household savings and government stimulus payments, many buyers had greater resources at hand to put money down toward a home–and they often needed to put more down to compete. As these trends have reversed, buyers are needing to borrow more to finance home purchases.

|

Read the full article here