GDP is the value of all goods and services produced in an economy, and in the U.S., its path since the onset of the COVID-19 pandemic provides the most basic measure of the virus’s impact on the economy. Although U.S. GDP has averaged an annual inflation-adjusted growth rate of over 3% since 1929, the pandemic caused historic drops in 2020. Real GDP dropped 2.7% from 2019 to 2020. Prior to 2020, the last time GDP fell was in 2009 during the Great Recession, decreasing 1.6% from 2008. And before that, a drop in GDP had not occurred since the early 1980s.

While U.S. GDP in aggregate decreased from 2019 to 2020, gross private domestic investments decreased by 5.5% and the trade deficit grew by 7.1%. Personal consumption expenditures decreased by 3.1%, while government consumption expenditures and gross investment actually increased by 3.2%. Fortunately, the U.S. is showing signs of recovery, with a 5.7% increase in GDP from 2020 to 2021, and a smaller yet still noteworthy 1.1% increase from 2021 to 2022.

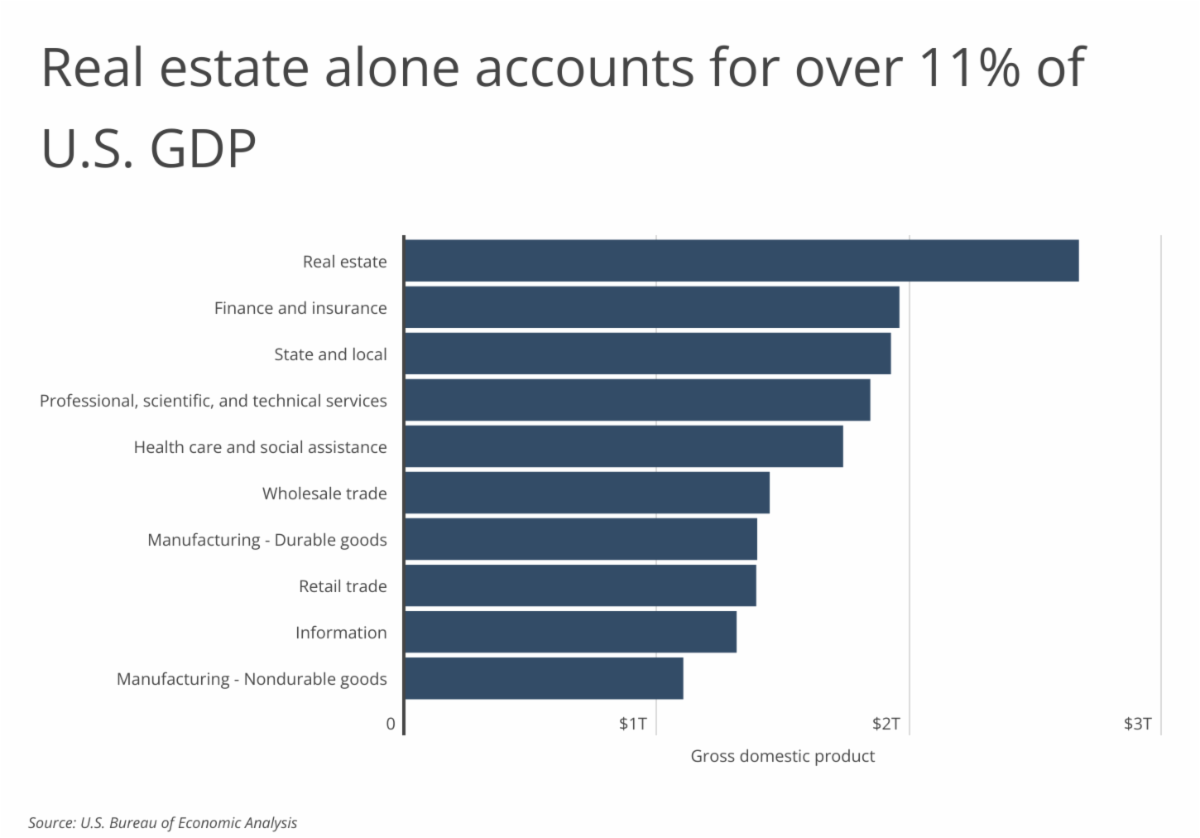

While total GDP includes consumer spending, business spending, government spending, and international trade, contributions to GDP vary widely by industry. In 2021, real estate alone accounted for over 11% of U.S. GDP, amounting to over $2.6 trillion in economic activity. The next largest industry was finance and insurance, which accounted for 8.4% of U.S. GDP. State and local government spending was not far behind in third, making up 8.3% of U.S. GDP. Manufacturing of non-durable goods contributed the least of all industry groups, but still made up 4.7% of U.S. GDP.

|

Read the full article here