Americans have increasingly turned to credit cards to meet their household financial needs—but doing so has dramatically raised risks of credit card fraud in recent years.

The early months of the COVID-19 pandemic saw many households reduce reliance on credit thanks to increased savings rates and government stimulus payments. Consumers paid off credit card balances at a record pace and applied for credit less often. But with high inflation over the past two years, Americans’ need for credit cards has rebounded as household costs have increased.

The aggregate, inflation-adjusted credit limit for newly issued consumer credit card accounts in the first quarter of 2020 was around $76 billion, but that figure fell by more than half to $35 billion in the second quarter of 2020 as pandemic lockdowns and stimulus measures took effect. Limits began to climb quickly again in 2021 as inflation took hold, and by the end of 2022, banks issued new consumer credit at the highest levels since 2016.

But with the rise in credit card usage comes increased risk for consumers as well—most notably from credit card fraud. Such fraud typically occurs in two forms: account takeover and application fraud. Account takeover fraud takes place when a bad actor obtains credentials or other personal information to gain access to the cards, funds, or other benefits associated with an existing account. Application fraud happens when a bad actor attempts to open new credit card accounts in another person’s name using personal information or counterfeit documents.

|

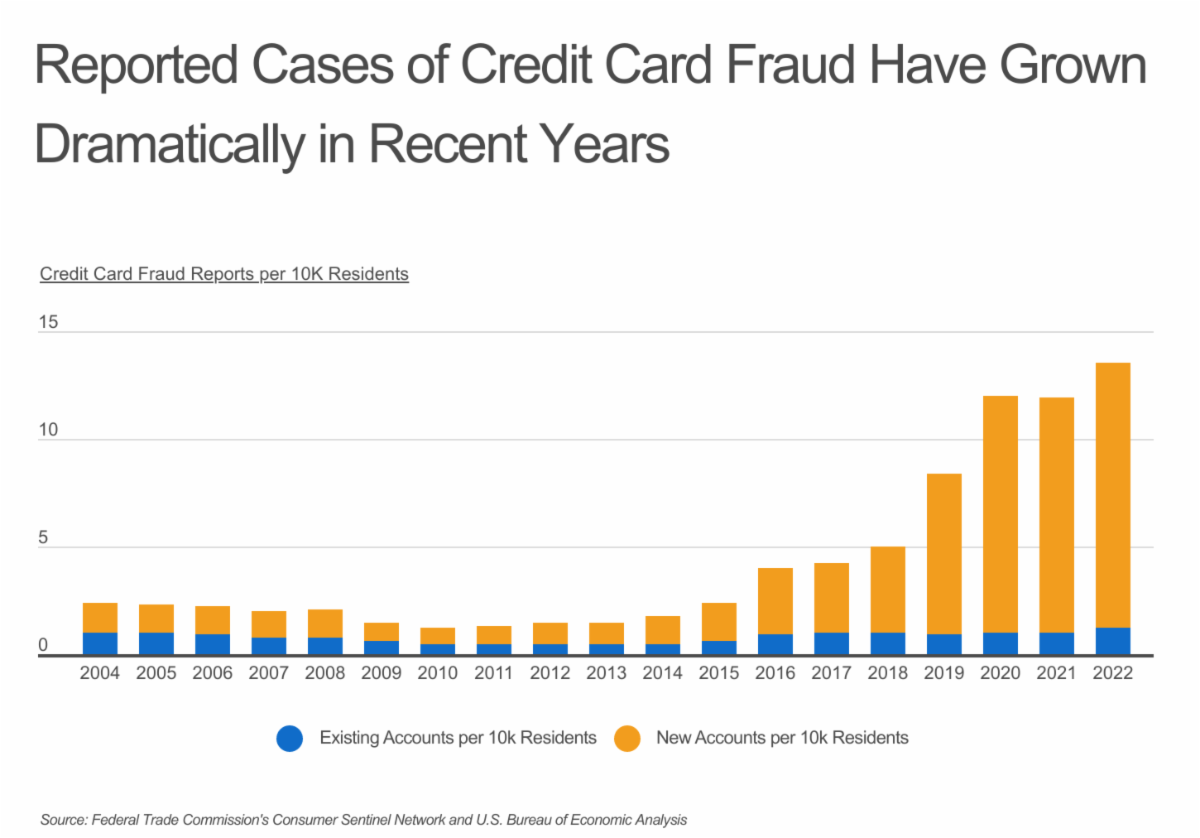

Credit card fraud has spiked overall, with reported fraud cases approximately tripling over the last five years. However, the bulk of the increase over time has come through application fraud. Reported cases of fraud from new accounts have risen tenfold within the last two decades, from 1.4 reports per 10,000 residents in 2004 to 14 per 10,000 in 2022. With phishing scams becoming more sophisticated…

Read the full article here